By Tim Estin, mba, gri with Coldwell Banker Mason Morse

By Tim Estin, mba, gri with Coldwell Banker Mason Morse

Q1 2013 Aspen Highlights:

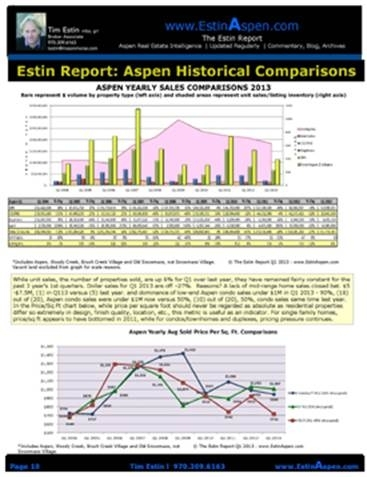

-In the 1st Quarter 2013 (Jan. 1- Mar. 31), the number of units, or properties, sold was up 6% from the same time last year, 90 units this year versus 64 last year, and dollar sales were down 23% at $148M this year versus $191M last year.

-A surge at the end of the year 2012 in big ticket $10M+ sales motivated by anticipated 2013 tax-changes seems to have taken the wind out of high-end Aspen dollar sales in the 1st Quarter 2013.

-Instead, market activity has been dominated by smaller-sized and under $1M property sales and a flood of new Snowmass Base Village Viceroy condo sales selling at 60% off pre- recession prices since their sales program was re-activated Dec. 15, 12 after a 3-year market hiatus due to litigation issues and the recession.

-Comparing the past three years 1st Quarters shows continued loss of dollar sales momentum from the recession high point in Q1 2011.

-Yet, in light of the positive trending economic news throughout the country - a record level stock market, strong real estate performance on both coasts and especially in NYC and the Hamptons - it is a puzzle why the Aspen market has not performed better in Q1 2013.

-Historically, the Aspen market has been last in, first out of recessions but presently, we appear to be trailing other high end markets.

-The big difference between this quarter and the same period last year is the significant increase in lower end sales under $1M, the lack of big ticket (+$10M) sales and a gaping hole of inactivity in the $5-10M sales range. The increase in lower end sales indicates a widening of Aspen’s real estate recovery base no longer limited to exclusively headline capturing high-end purchases.

__________________

The Estin Report: Q1 2013 State of the Aspen Real Estate Market Executive Summary

Click image or link to full report and charts pdf

Total Aspen Snowmass Market*

Q1 2013

In the 1st Quarter 2013 (Jan. 1- Mar. 31), the number of properties, or units, sold was up 6% from the same time last year, 90 units this year versus 64 last year, and dollar sales, the dollar value of all sales combined, were down 23% at $148M this year versus $191M last year.

A surge at the end of the year 2012 in big ticket $10M+ sales motivated by anticipated 2013 tax-changes seems to have taken the wind out of high-end Aspen sales in the 1st Quarter 2013. Instead, market activity has been dominated by smaller-sized and under $1M property sales and a flood of new Snowmass Base Village Viceroy condo sales selling at 60% off pre-recession prices since their sales program was re-activated Dec. 15, 12 after a 3-year market hiatus due to litigation issues and the recession.

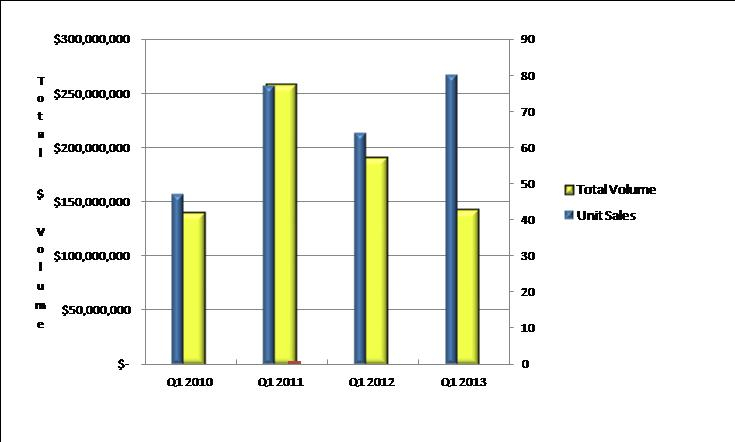

Prior Year 1st Quarter Comparisons

Aspen/Snowmass Total Sales by Qtr.

Q1 2013:

· $148M (-23% from Q1 2012)

· 90 unit sales (+41% from Q1 2012)

Q1 2012:

· $191M dollar sales (-26% from Q1 2011)

· 64 unit sales (-17% from Q1 2011)

Q1 2011:

· $258M dollar sales (+84% from Q1 2010)

· 77 unit sales (+64% from Q1 2010)

Q1 2010:

· $140M dollar sales

· 47 unit sales

©The Estin Report: Q1 2013 www.EstinAspen.com

*Total Market includes: Aspen with Brush Creek Village (BCV), Woody Creek (WC), Old Snowmass (OSM), and Snowmass Village (SMV), single family homes, condos/townhomes, duplexes and residential vacant land. All sold over $250,000. Fractional sales are not included

Comparing the past three years 1st Quarters shows continued loss of dollar sales momentum from the recession high point in Q1 2011.

Yet, in light of the positive trending economic news throughout the country - a record level stock market, strong real estate performance on both coasts and especially in NYC and the Hamptons - it is a puzzle why the Aspen market has not performed better in Q1 2013.

Historically, the Aspen market has been last in, first out of recessions but presently, we appear to be trailing other high end markets.

The big difference between this quarter and the same period last year is the significant increase in lower end sales under $1M, the lack of big ticket (+$10M) sales and a gaping hole of inactivity in the $5-10M sales range. The increase in lower end sales indicates a widening of Aspen’s real estate recovery base no longer limited to exclusively headline capturing high-end purchases.

The chart below illustrates the differences between this year and last two year’s distribution of Aspen unit sales by price which currently represent 76% of the total Aspen Snowmass market (does not include Snowmass):

When Q1 2013 is compared to sales in Q1 2011, the high-water mark for sales in a 1st Quarter during the past 4 years of the recession, the differences are even more profound. In Q1 2013, there were just 2 sales between $10M+ whereas in Q1 2011, there were 5 home sales above $10M+ (all built 2006 or newer and developer inventory was deeply discounted), a - 60% difference; and in the $5-10M category, there were just 2 sales in Q1 2013, versus 7 sales in Q1 2011 (all 2000 built or newer), a -57% difference.

Aspen Single Family Homes

The “best” neighborhoods, the Historic West End and Red Mountain, captured 60% of the single family home sales dollars in Q1 2013. But the Aspen Core or downtown area was relatively quiet this quarter realizing only 7% of the home sales.

Significantly smaller and generally, less expensive homes sold overall in Q1 2013 compared to Q1 2012. The average size of a sold Aspen single family home in Q1 2013 was 20% smaller than in Q1 2012, 3,535 sq. ft. now versus 4,427 sq. ft. then.

Price Ranges of Homes Sold

While there were 36% more homes sold under $5M in Q1 2013, (15) versus (11) in Q1 2012, there were 100% more, twice as many, homes sold under $4M in Q1 2013 over Q1 2012, (12) now versus (6) last year. In the middle range of $5M-$7.5M Aspen properties, there was just (1) sale at $5.3M in Q1 2013 versus (4) sales totaling $24.1M in Q1 2012, -78% less in dollar sales in this price category. In the over $5M price points, there were (3) home sales in Q1 2013 totaling $31.3M versus (6) sales over $5M in Q1 2012 totaling $47.9M, resulting in -35% less dollar sales.

Aspen Condos In Q1 2013, Aspen condo sales under $1M crushed all other sales categories: (18) out of total (20) Aspen condos, or 90%, closed under $1M, versus (10) out of a total (21) condo sales under $1M in Q1 2012, or 50%. Compare this low-end domination to sales in Q1 2011 - the 1st quarter recession’s highpoint - when just (5) Aspen condos closed under $1M out of a total (24) condo sales, or 21% - 90% of sales under $1M now vs. 21% then.

In Q1 2013, there was just (1) condo sale between $1-2M versus (11) in Q1 2011; in the over $2M category, there was just (1) sale in Q1 2013 at $7.5M for a downtown Aspen penthouse versus (8) condo sales over $2M in Q1 2011 with the (3) highest of these sales in the $4.3-4.7M range. What’s going on? The average sold Aspen condo in Q1 2013 was -52% smaller than those sold in Q1 2012, 908 sq. ft. now versus 1,903 then. As a result, all average and median prices were significantly lower, and dollar sales were off accordingly.

Vacant Land Sales Strong

There was a dramatic increase in vacant land sales in 2012 and lot sales have continued to be strong in Q1 2013 although at generally further reduced prices. The dollar volume of Q1 2013 lot sales is down -45% to $15M this quarter from $27M the same time last year. Builders/developers are chasing a depleting inventory of troubled land parcels, some still selling at significant discounts. Demand for land has accelerated for a number of reasons: 1) First and foremost, there is an absence of new built residential product on the market, and anything new - whether brand new or significantly remodeled, homes or condos - has been selling relatively quickly at premium pricing; 2) Generally lower land prices; 3) The low cost of capital; 4) A more competitive construction bidding environment and somewhat reduced labor costs though not material costs; 5) Faster time-to-build as the Pitkin County approval process has shortened the build-out timeline from 24-36 months during the boom days to approximately 18-24 months now.

At the same time, vacant land inventory is decreasing. The present 137 vacant land listings available now are roughly half, or 47%, of the Q1 2009 high point when the residential lot inventory reached 293 listings. Of particular note, the supply of high quality, A+ location lot/land listings is diminishing. And those special parcels that are available are achieving prices near their 2007/2008 peaks. (See Pg. 23).

SMV Single Family Homes

Sales of Snowmass homes remain moribund, at its lowest dollar volume level since 2004. But there has been activity in Sinclair Meadows, SMV’s newest sub-division which came online summer 2008 ...close to the worst time ever to launch sales. Sinclair home sites offer buyers the opportunity to buy 1/3 to 3/4 acre parcels and build a new home in the $2-3M range. This is the area to zero in on for new-built product at a relative discount. There have also been SMV home purchases under $1.5M perhaps being led by families seeking ‘affordable’ homes within the Aspen School District, rated #1 for Colorado by US World & News Reports.

SMV Condos - Viceroy Sales Dominate

In Q1 2013, Snowmass Village sold properties represents 24% of the total dollar volume of the combined Aspen Snowmass market. The resort has fallen on hard times in the past 4 years due to the Great Recession and the subsequent foreclosure and work stoppage of the Snowmass Base Village. After losing the project to a consortium of German banks, The Related Companies re-acquired the project on the cheap in the fall 2012.

In Dec. 2012, after settling 3 years of litigation by pre-construction buyers of the Viceroy Condo Hotel units for square footage misrepresentation, the Viceroy sales program rebooted offering Snowmass resort’s newest 2010 built, ski in/out condos at 60% off pre-recession prices. Buyers have recognized the value, and the results have been astounding.

· In Q1 2013, 24 of the 34 total SMV condos sales, or 71% of all condo sales, were Viceroys. Viceroy sales totaled $12.6M, or 55%, of the total $23.1 SMV condo sales and 60% of all SMV units sold (condos, homes, vacant lots).

· Eight out of every ten ski in/out SMV condo sales have been Viceroy units.

· There were (18) Viceroy studios and 1-bedrooms that sold at an average $742 sq. ft., and there were (5) 2-bedroom sales at an avg. $1,053 sq. ft.

For a perspective on the rest of the SMV condo market, in Q1 2013, there were (10) non-Viceroy SMV condo sales for a total $10.5M dollar sales versus (7) total SMV condo sales for a total of $6.1M dollar sales in Q1 2012.

SMV Good News

Unbelievable deals are to be had in Snowmass Village and buyers are urged to investigate the highly discounted property opportunities in this very beautiful area so close to Aspen.

Of general note, the primary Snowmass Village real estate selling season is winter/spring due to the prevalence of ski-in/ski-out properties that characterize the resort. Consequently, summer and fall transaction activity drops off dramatically and there may be greater 'deal' opportunities to purchase then as owners do not wish to wait for, or possibly endure, another winter of property carrying costs.

__________________

Disclaimer: The statements made in The Estin Report represent the opinions of the author and they should not be relied upon exclusively to make real estate decisions. Information concerning particular real estate opportunities can be requested from Tim Estin at 970.920.7387 or by email. A potential buyer is advised to make an independent investigation of the market and of each property before deciding to purchase. To the extent the statements made herein report facts or conclusions drawn from other sources, the information is believed by the author to be reliable. However, the author makes no guarantee concerning the accuracy of the facts and conclusions reported herein. The Estin Report is copyrighted 2013 and all rights are reserved. Use is permitted subject to the following attribution: "The Estin Report by Aspen broker Tim Estin mba, gri" www.EstinAspen.com